Prepare to raise | CORE

Expert guidance, investor matching, and visibility

Private rounds

Raise from your network with professional infrastructure

Cap table & equity management

All-in-one equity and stakeholder management

ESOP

Incentivize your employees and manage ESOPs seamlessly

Explore SeedBlink Legal

Industry trends

Discover the latest fundraising insights in European venture that influenced the first quarter of this year.

May 15, 2026

·

4

min read

%20-%20Q1%202026%20-v2.2.png)

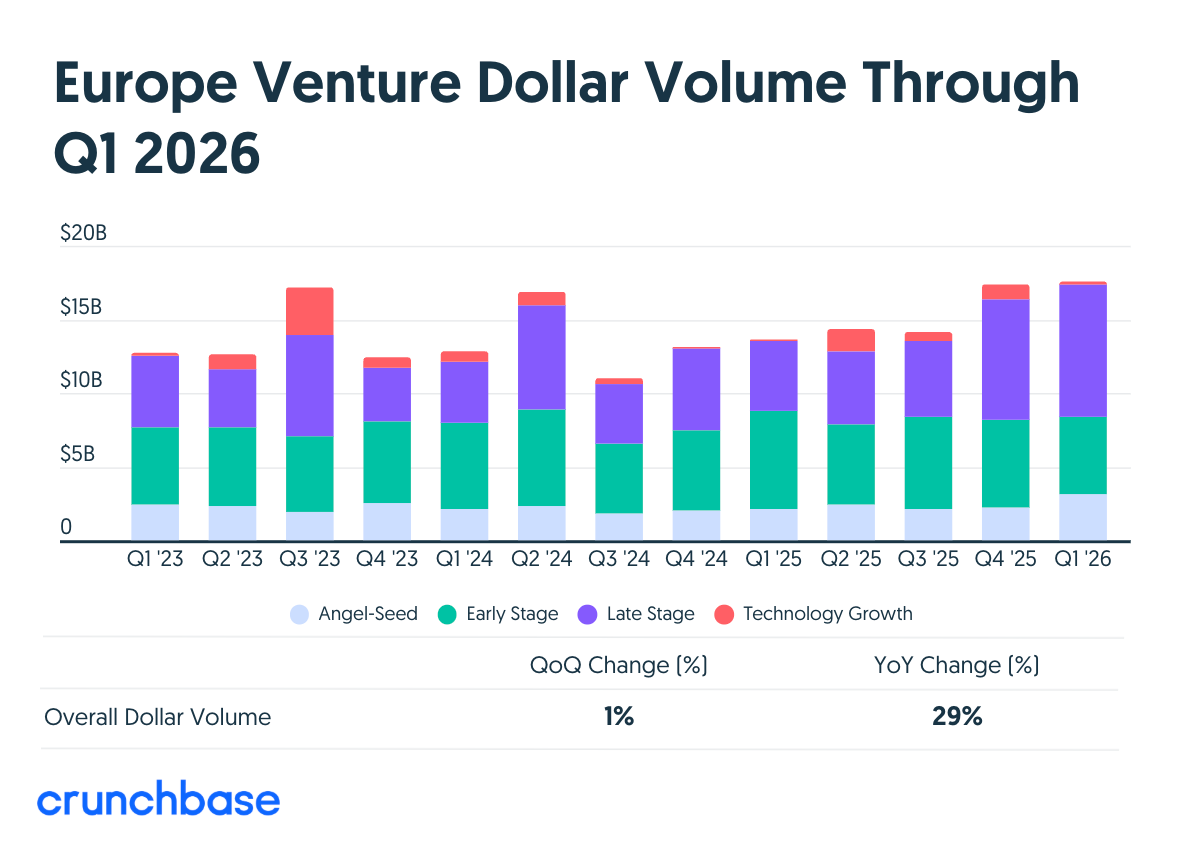

In Q1 2026, European venture capital funding remains available despite a more selective market environment. While total deal value was supported by several large financings, overall deal count declined, with investors concentrating capital into fewer companies and larger late-stage rounds. Fundraising also showed only early signs of recovery after a weak 2025, remaining well below the highs seen in 2021 and 2022.

At the same time, several sectors and regions continued to stand out. AI is the star of this quarter, accounting for more than 60% of total deal value and producing nine of the ten largest rounds. Late-stage funding nearly doubled year over year, while DACH emerged as one of the strongest regional performers, supported by major rounds in robotics, AI, and industrial technology. Nontraditional investors, including hedge funds and corporate VCs, also played a growing role in the market.

In this article, we break down the most important trends and reports from the first quarter of 2026, including deal activity, fundraising trends, regional performance, sector highlights, and the investors shaping Europe’s venture market.

Europe’s venture market in Q1 2026 shows that money is still available, but it is reaching fewer companies. Total funding increased by 29% from a year earlier and was slightly higher than the previous quarter, mainly due to larger late-stage and growth-stage rounds.

At the same time, total deal count dropped 40% year over year and 13% quarter over quarter, meaning many startups were unable to raise capital. The biggest slowdown was at the angel-seed stage, where deals fell 44%, followed by early-stage deals, down 30%, while late-stage activity stayed relatively steady.

This points to a more cautious investment environment, where investors prefer backing established companies with clearer traction rather than taking risks on younger startups.

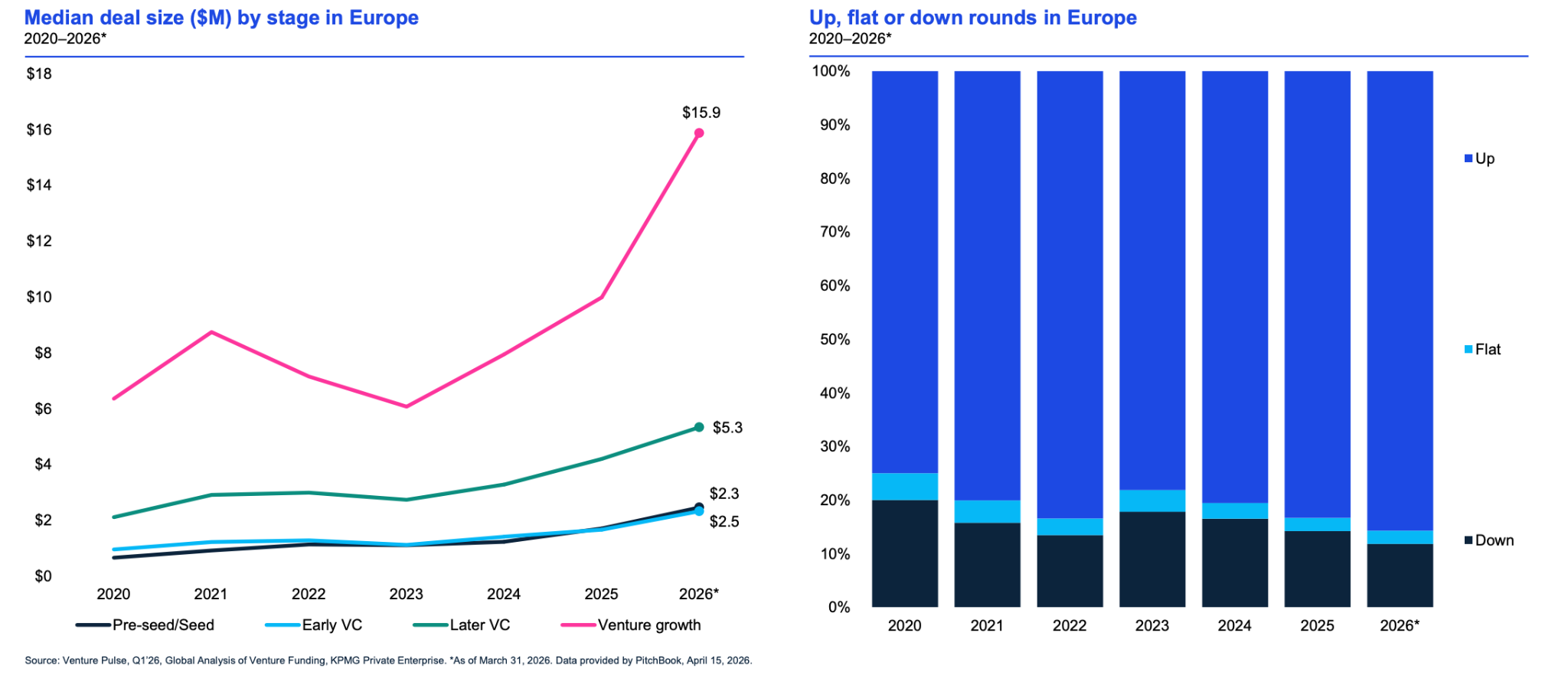

Europe’s venture market in 2026 shows continued pricing strength across nearly all funding stages, while down rounds remain relatively limited. Median deal sizes have increased from 2020 levels, with the strongest gains at later stages, where venture growth rounds reached $15.9M, later VC climbed to $5.3M, and early VC rose to around $2.3M.

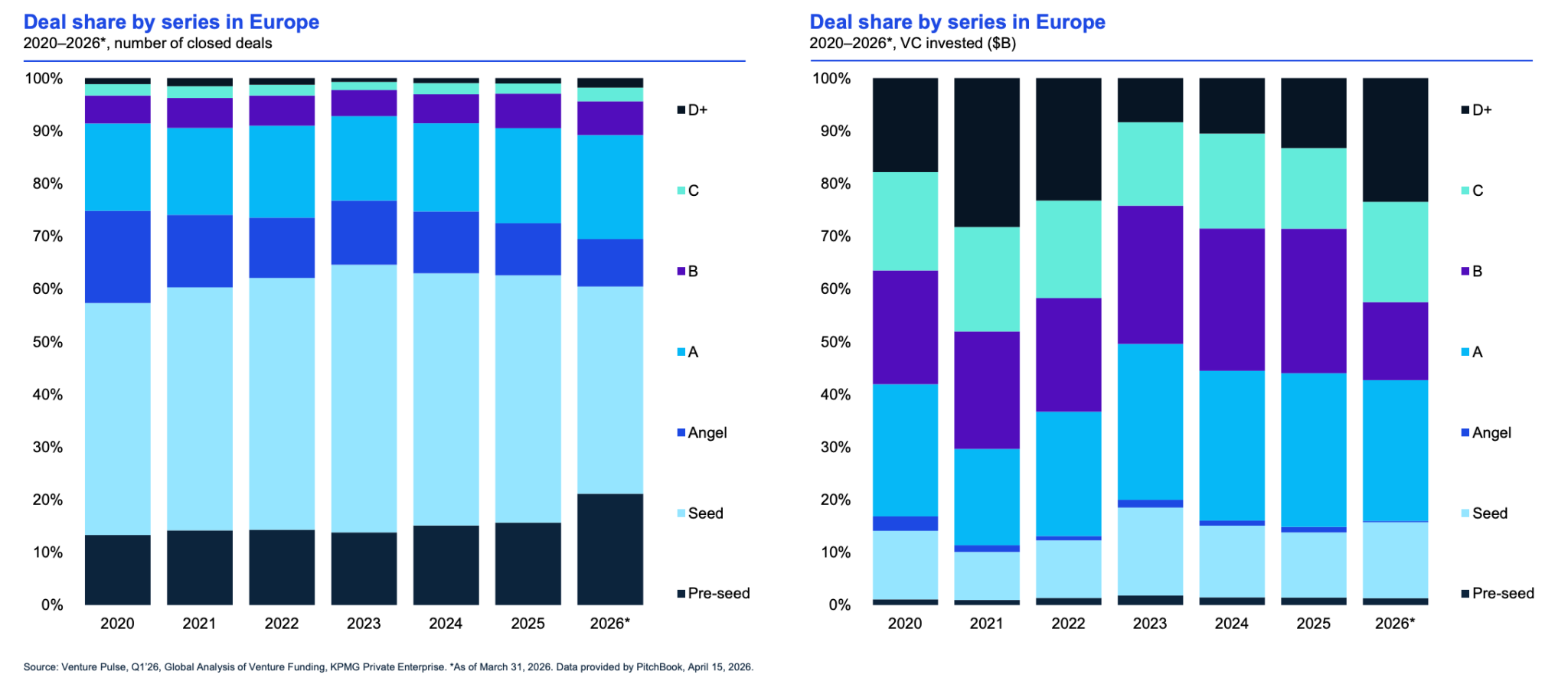

Across named series rounds, larger financings remain especially strong, with median D+ rounds jumping to $200.4M, Series C reaching $75M, and Series B at $35.5M. This suggests that investors are still willing to deploy meaningful capital into companies that have proven scale, revenue traction, or strategic importance, even in a more selective market environment.

At the same time, the market remains clearly split between the earliest and latest stages. By number of deals, seed and pre-seed rounds continue to account for the majority of transactions, indicating that startup formation and early fundraising activity remain active. However, by dollars invested, later-stage rounds such as Series B, C, and D+ capture a much larger share of total capital.

This means many smaller, early-stage companies are still getting funded, but most of the money is flowing to a narrower group of mature startups. Overall, Europe’s venture ecosystem appears healthy in activity, but capital concentration at the top end continues to widen.

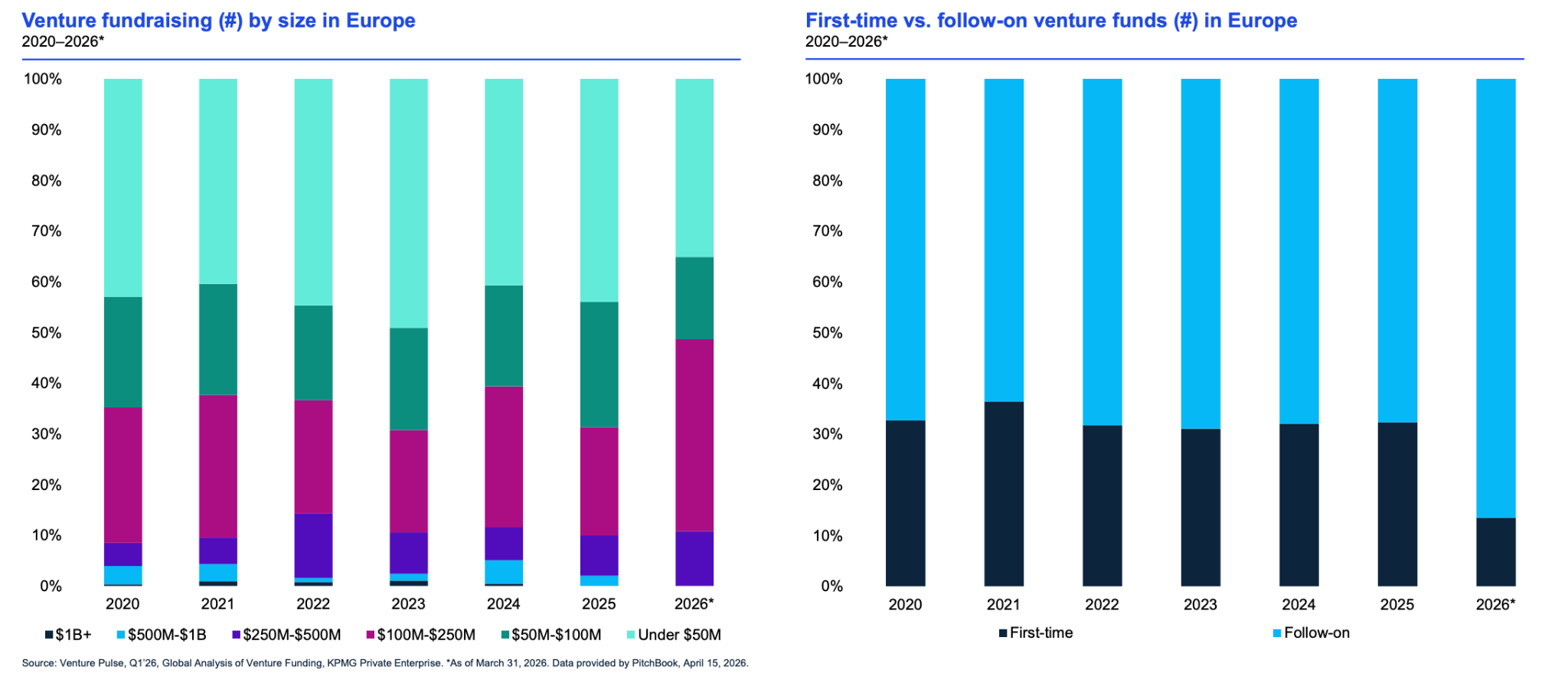

Europe’s VC fundraising market is showing early signs of recovery in 2026, following a record low in 2025. Funds raised reached €3.5B in Q1 across 37 vehicles, putting the market on pace for roughly 11% year-over-year growth if momentum continues. However, activity remains well below the 2021–2022 peak, when annual fundraising exceeded €32B and fund counts were significantly higher.

European VC fundraising remains under pressure in 2026, showing that LP confidence has not fully returned despite a modest rebound in capital raised. After the $42.4B highlight in 2022, fundraising fell to $14.1B in 2025, with only $4.1B raised in Q1 2026. Fund counts have also continued to decline, highlighting weaker overall market enthusiasm.

The current environment favors established managers, as follow-on funds account for the large majority of new vehicles, while first-time funds dropped to roughly 13% of total launches in Q1 2026, their lowest share in years. Fund sizes are also shifting toward the middle market, with more activity in the $100M to $250M range, while mega-funds remain limited.

For a closer look at where momentum is building, read our full article covering the venture funds raised in Europe during the first quarter of 2026.

European VC deal activity in Q1 2026 highlights a market where capital remains concentrated despite lower transaction volume. Total deal value reached €21.9 billion in the first quarter, while estimated deal count stood at 2,805, indicating that investors completed fewer transactions but committed larger amounts per round. It reflects an ongoing value-over-volume trend, where capital is flowing into a smaller number of high-conviction companies rather than being spread broadly across the ecosystem.

Compared with recent years, deal volume remains well below the 2021 peak, but funding levels are being supported by larger late-stage financings.

AI was the dominant factor behind these trends, accounting for 61.3% of all European VC deal value in Q1, far above the 37.7% share recorded at the end of 2025. And nine of the top ten deals in the quarter were AI companies.

The broader funding mix also points to a late-stage bias. Rounds above €25M represented 79.2% of total deal value in Q1, up sharply from 67.1% in 2025, with Series D+ rounds gaining share while Series B lost ground.

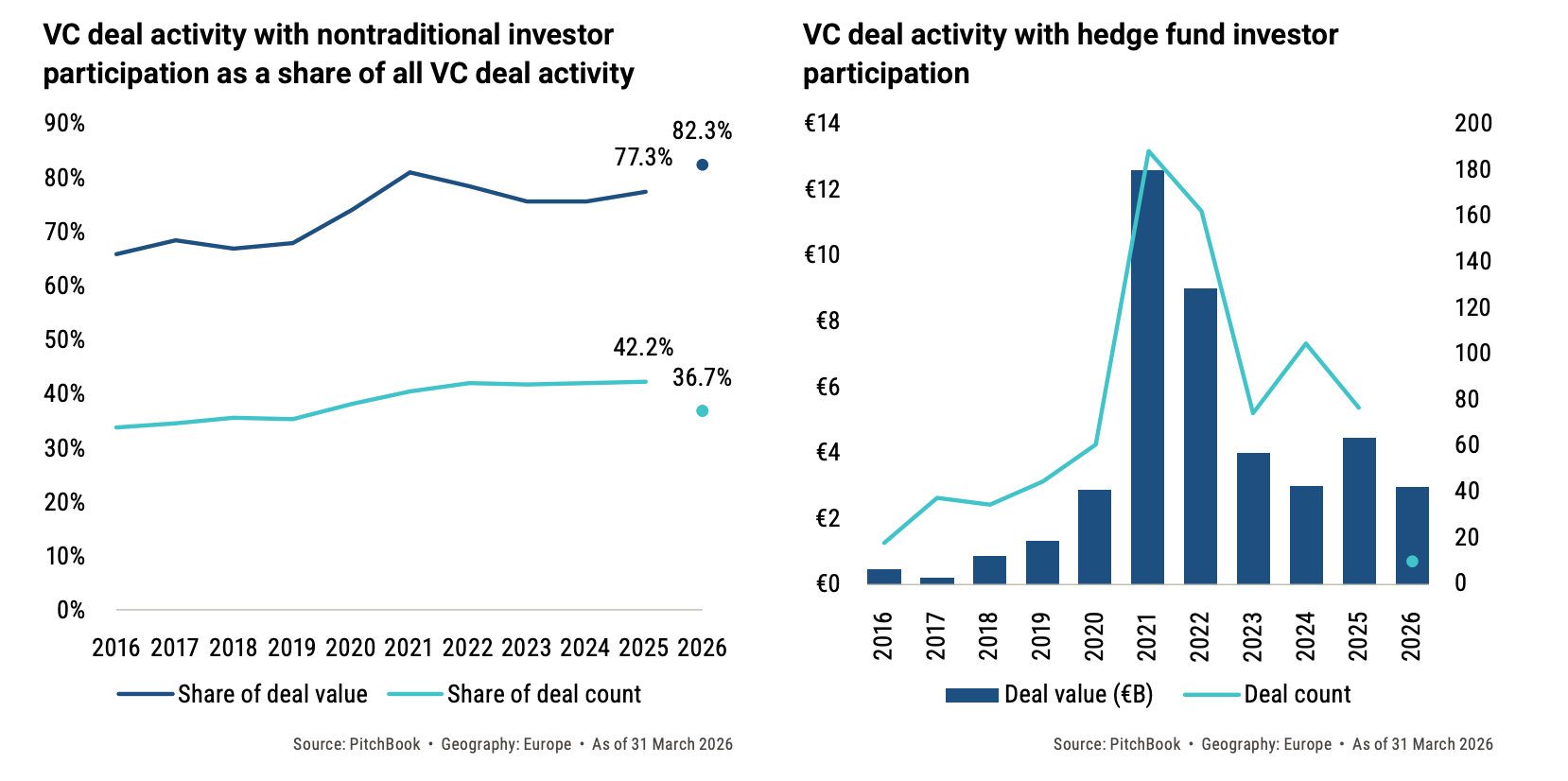

Nontraditional investors also played an important role, participating in 82.3% of total deal value, an all-time high, while hedge funds alone deployed around €3 billion, and corporate venture investors remained highly active.

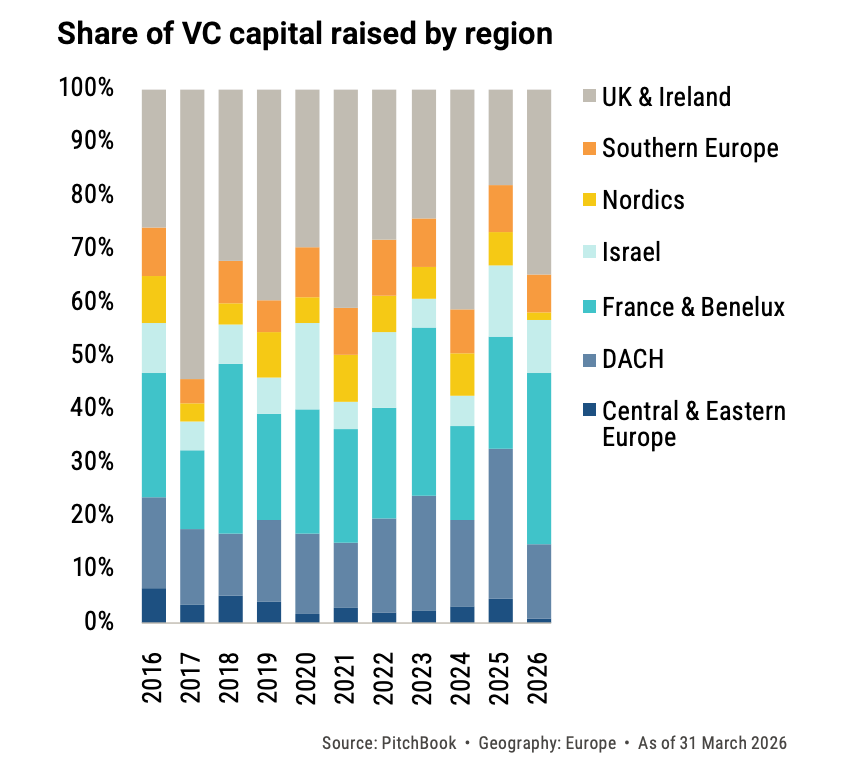

In Q1 2026, the top three European regions for VC fundraising were the UK & Ireland, France & Benelux, and DACH. UK & Ireland regained the leading position with 34.8% of total capital raised, reinforcing London’s role as Europe’s main fundraising hub. France & Benelux followed closely with a similar share, supported by several large fund closes in Paris and strong momentum across the broader region.

DACH ranked third, but with a much smaller 11.1% share, showing that while the region remained active in the number of fund closes, smaller average fund sizes limited total capital raised.

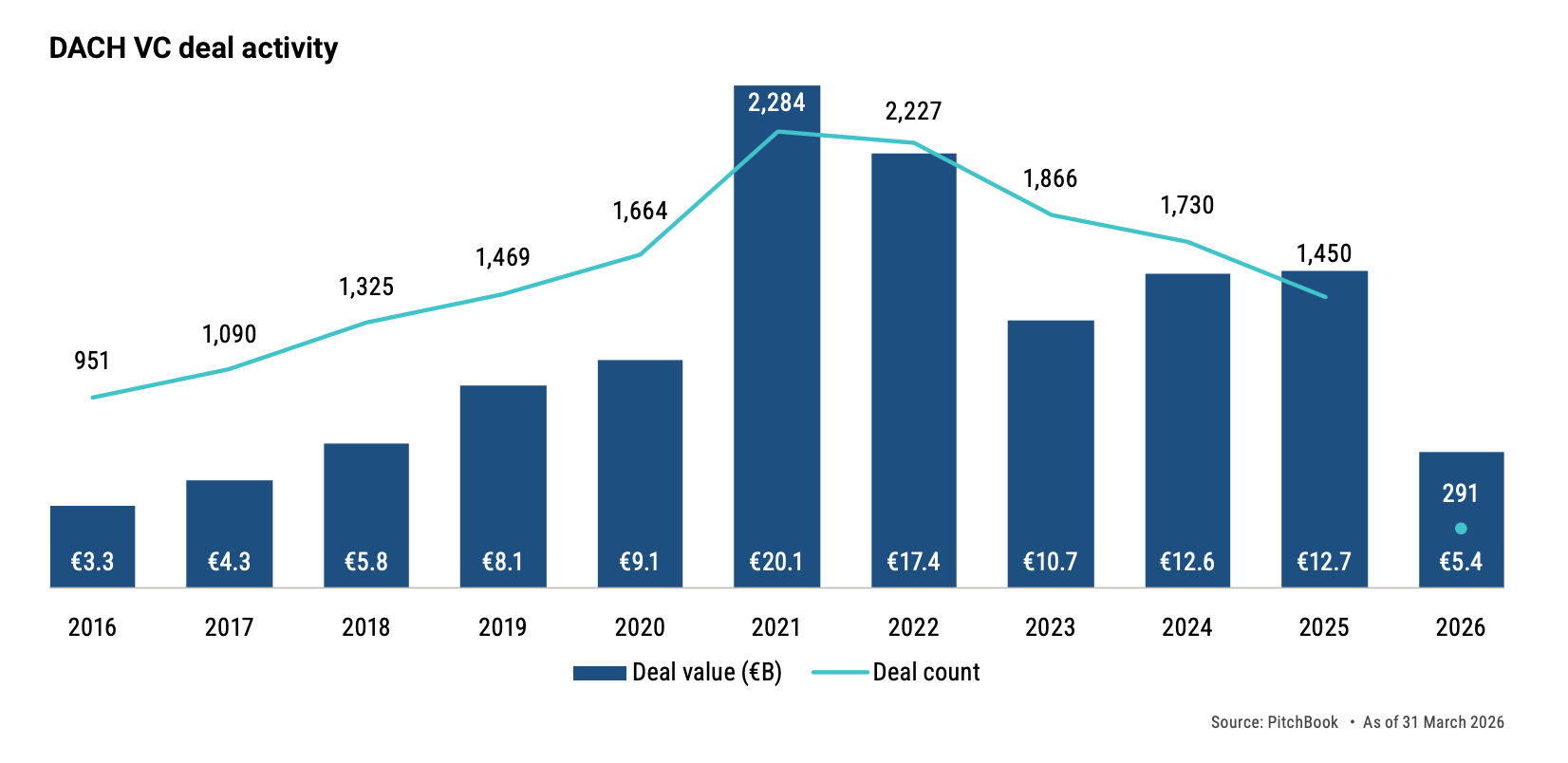

However, in terms of deal activity, the region has emerged as Europe’s strongest-performing VC region in the first quarter, raising €5.4 billion by the end of March, already nearly half of its full-year 2025 total.

The surge was driven by several large transactions, including major rounds like NEURA Robotics, with additional €200 million-plus deals supporting momentum across Germany and Switzerland. While AI remained a main driver of the largest financings, the fact that half of the top 10 rounds were outside AI suggests investment strength is broadening across sectors.

In contrast, regions that were stronger in 2025, such as France, Israel, Southern Europe, and the Nordics, started the year more slowly, with fewer large rounds and smaller ticket sizes. Overall, the data shows investors concentrating capital in DACH as a region offering both scale opportunities and deeper sector diversity.

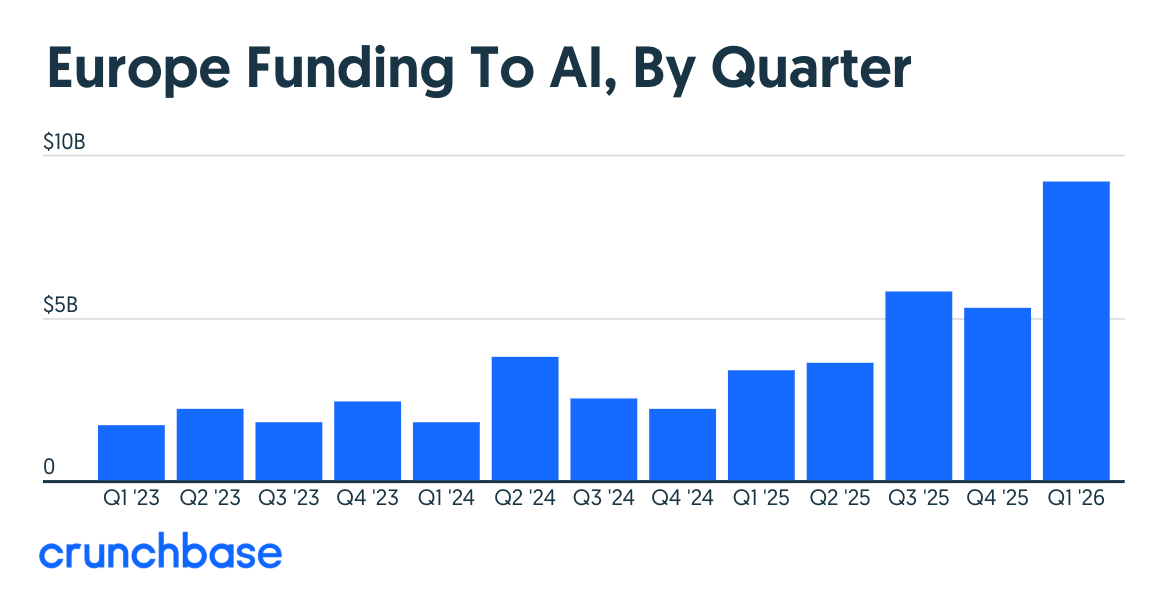

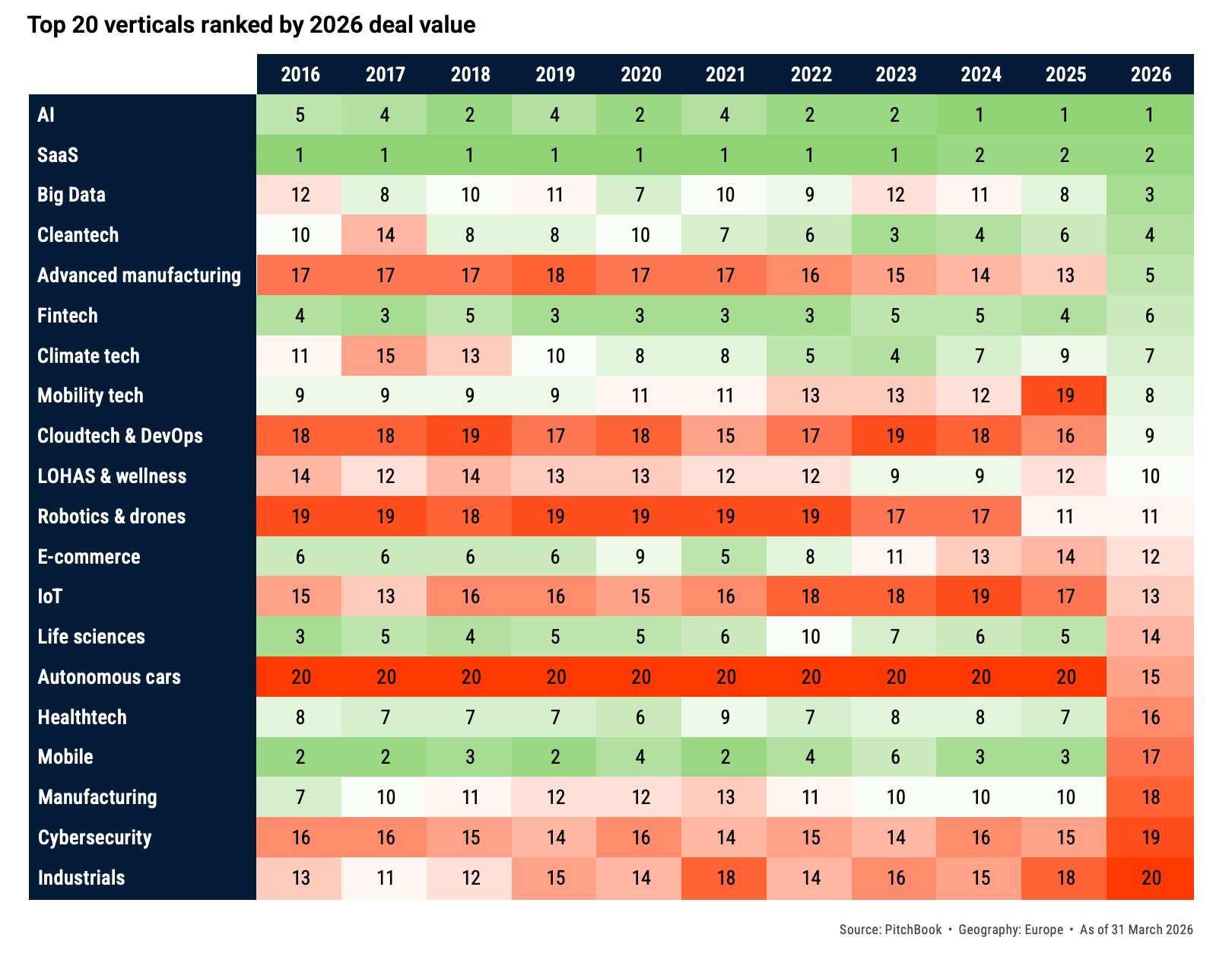

AI was by far the strongest industry for European venture funding in Q1 2026, ranking first and attracting $9.2B, more than 50% of all venture capital invested in the region. This marks the highest quarterly share on record and shows how strongly investor attention has shifted toward artificial intelligence.

The largest four rounds in Europe during the quarter were all AI-related, and demand is being driven by investor appetite for foundational models, applied AI software, autonomous systems, and the infrastructure needed to support the next wave of computing.

Behind AI, SaaS ranked second, and Big Data placed third, showing that software remains a core part of Europe’s venture ecosystem. SaaS continues to attract steady funding because of recurring revenue models and clear paths to scale, while Big Data benefits from rising enterprise demand for analytics, automation, and data infrastructure.

Together, these top three sectors highlight where investors currently see the strongest growth potential: AI as the breakout category, supported by resilient software and data platforms that help businesses adopt and monetize new technologies.

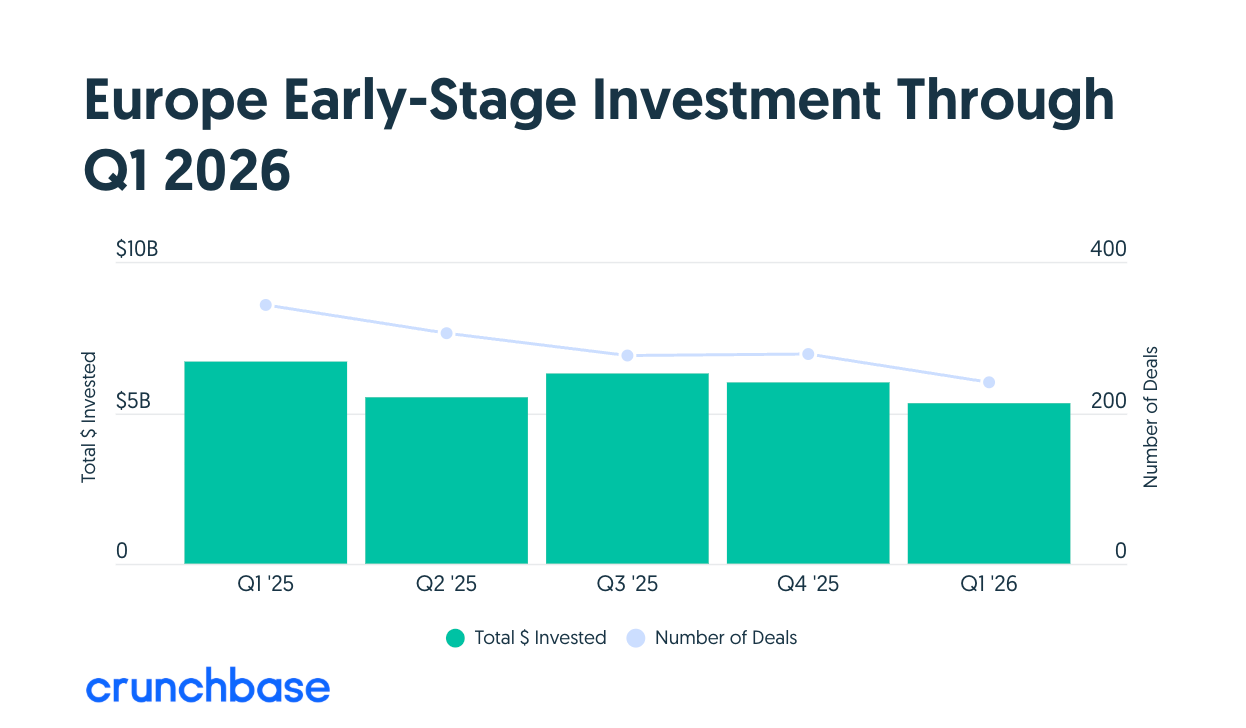

Europe’s startup funding picture in Q1 2026 shows a split between maturing companies and the earliest stages. Early-stage investment fell about 20% year over year to $5.3B across more than 240 rounds, with deal volume also trending lower, suggesting investors are becoming more selective and concentrating larger Series A checks into capital-intensive sectors such as semiconductors, energy, and healthcare.

At the same time, seed and angel funding increased up to $3.1B across more than 790 deals, up 50% from a year earlier, although this increase was heavily influenced by a single $1B round, according to Crunchbase. Excluding that outlier, seed activity appears healthier in volume than in value, indicating continued appetite for new startup creation but tighter pricing discipline.

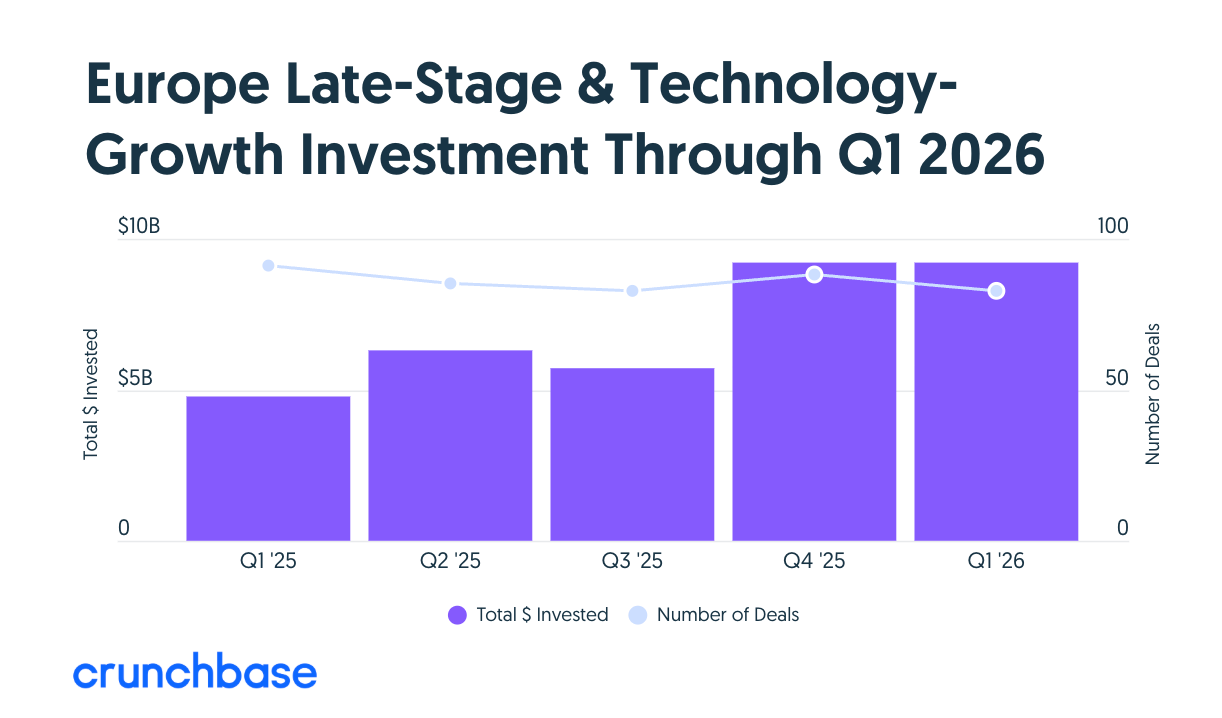

European late-stage venture funding delivered one of the strongest performances in Q1 2026, with $9.2 billion invested across 83 deals, marking a 91% year-over-year increase. The sharp rise shows that investors are deploying larger checks into more mature startups with proven traction, even as earlier-stage markets remain more selective.

Capital was spread across a broad mix of sectors, including AI hardware, fintech, agentic AI, productivity software, sensors, defense, e-commerce, and energy, underscoring that late-stage demand is not limited to a single theme.

Overall, the quarter suggests institutional investors are regaining confidence in scaled European companies, particularly those positioned for growth, strategic relevance, or near-term profitability.

As we have already seen, the first quarter indicates that the current state of the market calls for better preparation and less ambiguity in growth strategies.

Most of the funding is going to companies that already show customer demand. Seed activity is still happening, new companies are still being funded, and more types of investors are entering the market, including hedge funds and corporate investors.

In 2026, founders who are prepared, focused, and able to show steady growth will have a better chance of raising capital. Fundraising may take longer, and investors may ask tougher questions, but strong startups solving real problems can still stand out and secure meaningful funding.

If you want to connect with VC funds or check out other active investors in the region, check out SeedBlink’s European VC Network list covering venture capital funds from SEE, DACH, Benelux, and others.

Want to secure a larger investment from multiple angel investors? Consider more flexible funding options for your next round, such as SeedBlink's syndicate infrastructure and rolling facility, which enable continuous fundraising.

Written by

Patricia Borlovan

Communication Specialist

TABLE OF CONTENT

Subscribe to our newsletter

No spam. Just the latest releases and tips, interesting articles, and exclusive interviews in your inbox every week.

Share this article

The latest news, technologies, and resources from our team.

%20-%20Ready%20to%20invest_%20European%20VC_Q1%202026.png)

%20-%20Spain%20(angels%20%2B%20investors)%202.png)

%20-%20V1.4.2.png)

%20-%20Andrei%20Hancu%203.png)

%20-%20mir_detect.png)

%20-%20moneco%202.png)